TABLE OF CONTENT

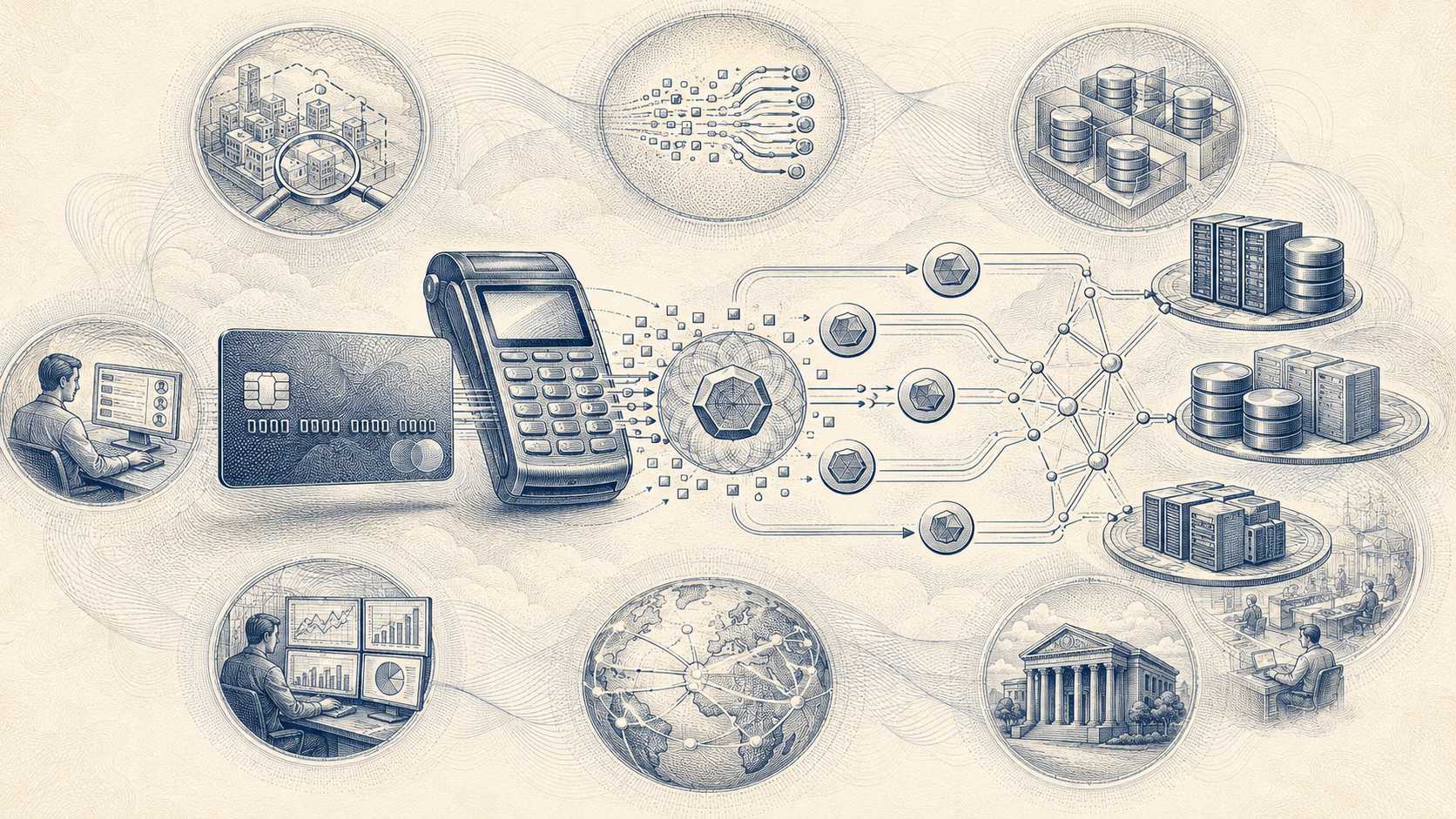

Tokenization is a process where sensitive payment information—such as a Primary Account Number (PAN)—is replaced with a unique, randomly generated placeholder called a "token." These tokens cannot be mathematically reversed to recover the original data. Instead, the true sensitive data is securely stored in an isolated token vault managed by a PCI DSS-compliant provider, ensuring that the critical information remains entirely outside the organization’s operational systems.

Unlike encryption, where data can be decrypted directly if an attacker possesses the correct cryptographic key, tokenization ensures that the sensitive data simply does not exist within the business’s environment. For example, when a customer’s credit card is swiped or entered online, the PAN is tokenized immediately. The token safely flows through the system for processing and analytics. This approach drastically shrinks the attack surface, providing a critical layer of defense against modern cyber threats.

5 Major Benefits of PCI DSS Tokenization

Tokenization offers a vast range of strategic advantages for businesses operating in the payment industry:

- Enhanced Security: Tokens are meaningless strings of characters outside the specific proprietary system they were created for. If hackers breach your local network, the tokens they steal are entirely useless.

- Simplified Compliance Scope: By replacing actual PANs with tokens, organizations drastically reduce the footprint of their Cardholder Data Environment (CDE). This removes entire systems from the scope of PCI DSS requirements, making audits faster and less expensive.

- Cost Efficiency: A smaller audit scope means fewer systems require expensive, rigorous security controls. These massive cost savings allow organizations to reinvest in strategic growth areas.

- Seamless Operational Utility: Tokenization safely streamlines internal processes such as recurring billing, loyalty programs, and data analytics. Because tokens often retain the format of the original data (e.g., a 16-digit number), they integrate seamlessly with legacy billing systems without causing operational disruptions.

- Elevated Customer Trust: Demonstrating advanced, frictionless security practices enhances customer confidence. Knowing their data is never directly stored on your servers builds lasting brand reputation.

Strict PCI DSS Tokenization Guidelines

Tokenization is not a silver bullet unless implemented correctly. Adhering to PCI DSS guidelines ensures the solution is secure, compliant, and resilient:

- Tokenization and De-tokenization Security: The processes for generating and reversing tokens must be heavily secured. Regular audits must be performed to validate the integrity of the token mapping process.

- Secure Infrastructure: Tokenization systems must reside in highly segmented, PCI-compliant environments that are completely isolated from untrusted networks.

- Strong Cryptography: While the token itself is not encrypted data, the vault storing the original PAN must be protected using robust, industry-standard cryptographic algorithms for both storage and transmission.

- Access Control and Monitoring: Organizations must implement strict role-based access controls and continuous monitoring. Only authorized personnel should be able to trigger a de-tokenization request.

- Third-Party Vendor Compliance: If you outsource tokenization to a third-party vault provider, you must ensure they actively maintain their own PCI DSS compliance. You are required to review their compliance attestations (AOC) annually.

- Card Data Vault Security: The vault storing the original data is the ultimate target for attackers. It requires aggressive controls, secure deletion policies, and frequent infrastructure and network penetration testing to continuously identify and address potential vulnerabilities.

How Tokenization Reduces PCI DSS Compliance Scope

The most immediate financial and operational benefit of tokenization is its ability to minimize your PCI DSS compliance scope. When a business does not hold the actual PAN, the systems processing the token are largely removed from the stringent requirements of the PCI DSS framework.

For example:

- Tokens replace PANs during transactions, actively shrinking the Cardholder Data Environment (CDE). The exposure of sensitive data is confined entirely to the highly controlled token vault.

- Merchants utilizing tokenization no longer need to worry about inadvertently storing sensitive authentication data (SAD) like CVVs or magnetic stripe data. Leveraging advanced data discovery and classification tools alongside tokenization ensures no "shadow" card data is left behind on your network to trigger an audit failure.

- By outsourcing the vault to a trusted third-party provider, businesses transfer a massive portion of the compliance burden, allowing internal teams to focus on core operations.

Tokenization vs. Encryption: What is the Difference?

Though both secure sensitive data, they function fundamentally differently:

- Tokenization replaces data with a non-mathematical placeholder. It cannot be reversed without direct access to the heavily guarded token vault.

- Encryption transforms data using a mathematical algorithm and a cryptographic key. If an attacker steals the key, they can decrypt the data directly on your servers.

While encryption is absolutely essential for data in transit, tokenization is vastly superior for data at rest, as it removes the risk of decryption from your local environment entirely.

Best Practices for Implementing Tokenization

- Choose the Right Provider: Partner with a proven, PCI-compliant provider that offers secure token vault management and has a flawless track record.

- Define Your Scope Clearly: Evaluate exactly how tokenization alters your network architecture. Document these boundaries meticulously to support your QSA during audits.

- Integrate Role-Based Access: Heavily restrict who (and what applications) can request the de-tokenization of sensitive information.

- Engage Continuous Support: Tokenization simplifies compliance, but it does not eliminate it. Utilizing expert managed compliance services ensures your segmented environment, access controls, and vendor attestations remain audit-ready 365 days a year.

Conclusion

PCI DSS tokenization is a transformative tool for enhancing payment security while simultaneously neutralizing the heavy burden of compliance. By removing sensitive cardholder data from your network entirely, your organization reduces its risk exposure, slashes audit costs, and provides a frictionless, highly secure experience for your customers. Adopting tokenization is no longer just a compliance tactic—it is the cornerstone of modern, defensible payment architecture.

Frequently Asked Questions (FAQs)

Does tokenization mean I am completely exempt from PCI DSS compliance?

No. While tokenization drastically reduces the scope of your Cardholder Data Environment (CDE) and simplifies your audit, your organization must still validate that the systems interacting with the token provider are secure. You are also required to verify the compliance status of your third-party tokenization vendor annually.

Can a token be hacked or reversed?

A true token has no mathematical relationship to the original Primary Account Number (PAN). Therefore, it cannot be "decrypted" or reversed mathematically by a hacker. The only way to retrieve the original data is to breach the highly secure, isolated third-party token vault and successfully map the token back to the PAN.

Is tokenization only useful for credit card numbers?

No. While it is heavily utilized for PCI DSS compliance to secure credit card PANs, tokenization is increasingly used to protect Personally Identifiable Information (PII), Protected Health Information (PHI), bank account numbers, and other sensitive corporate data to meet broader privacy regulations like GDPR and DPDPA.

Why is tokenization better for recurring billing than encryption?

With encryption, the merchant must securely store the encrypted credit card data and manage the decryption keys locally, which keeps their entire server in scope for a PCI audit. With tokenization, the merchant simply stores the token. When it is time to bill the customer, the merchant sends the token to the payment processor, who matches it to the real card in their secure vault and processes the payment, keeping the merchant's servers out of scope.