Storing tokens instead of PANs is an alternative to reduce the amount of cardholder data in the environment and helps in reducing the merchant’s effort to implement PCI DSS 4.0 requirements. Besides, by eliminating the need to store actual card numbers, tokenization can significantly reduce the risk of data breaches.

TABLE OF CONTENT

Card payments have become an integral part of our daily lives, enabling seamless transactions and convenient purchases across global networks. However, with the exponential rise of digital transactions, severe security concerns have grown in parallel. The risk of devastating data breaches and fraudulent activities looms over every payment made with a credit or debit card.

The PCI-DSS compliance framework revolves around the absolute security of the Primary Account Number (PAN) along with other sensitive authentication data (SAD), which is considered the crown jewel in any payment transaction. Cybercriminals can compromise these data elements while they are being stored, processed, or actively transmitted across networks.

Protecting this key data element by implementing a defense-in-depth strategy is critical to securing card payments. In this blog, we will look at how tokenization—a powerful security measure and a strict regulatory requirement mandated by most central banks—can help significantly reduce this operational risk.

Understanding Tokenization

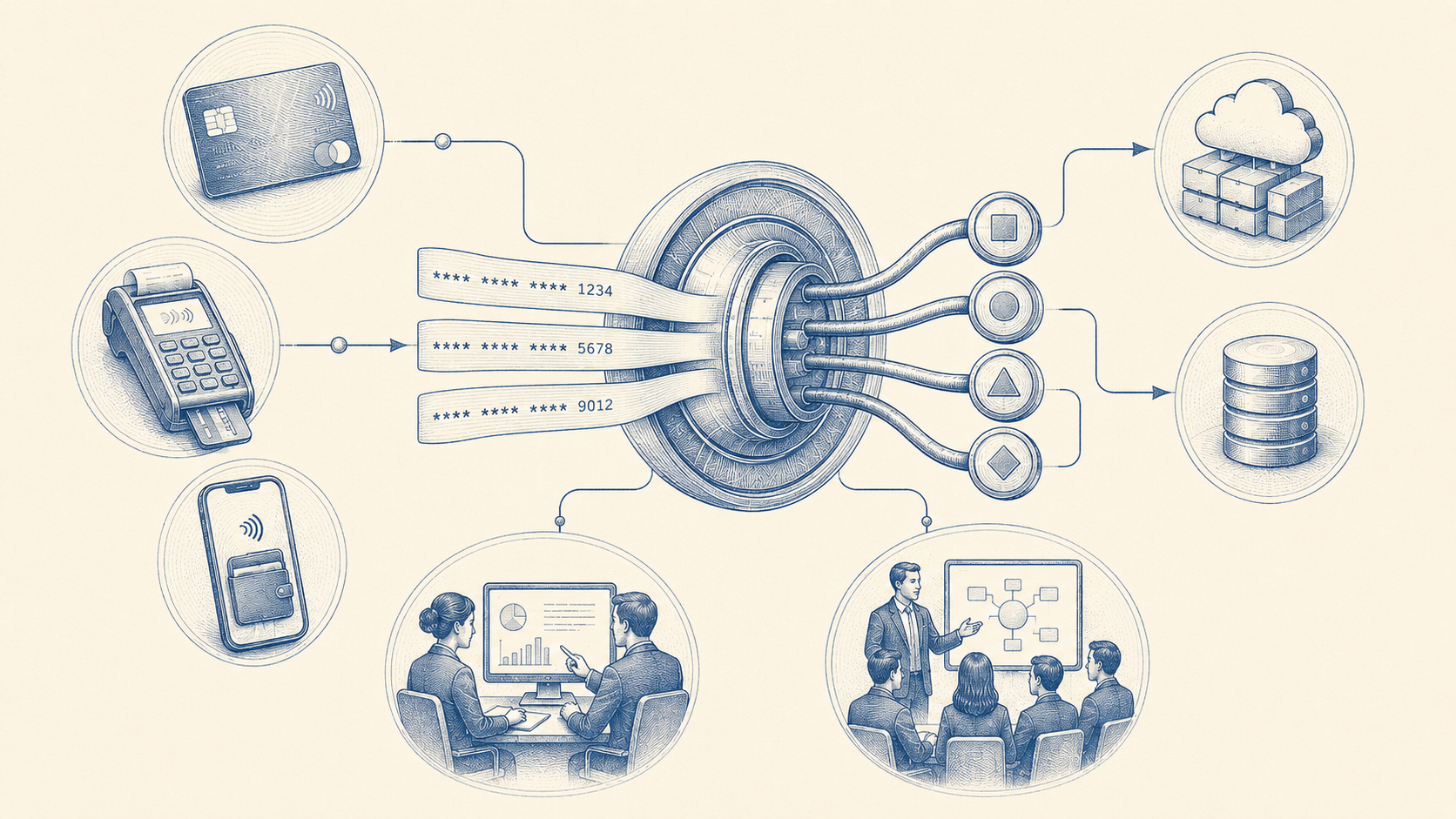

Tokenization is an advanced cryptographic process that replaces highly sensitive payment information, such as the actual PAN, with a surrogate value (a random alphanumeric number) called a “Token.” Converting a PAN into a token is the process of tokenization.

Payment tokens are automatically issued in real-time and used online in pre-defined domains or secure payment environments. Examples include tokens generated exclusively for e-commerce, restricted to specific merchants, or bound to a specific mobile device (like Apple Pay). The token has absolutely no meaning or value outside of the specific payment system. Even if an attacker successfully captures the payment traffic and accesses the token, it is non-sensitive and entirely useless to them. These tokens are then routed to authorize the transaction instead of transmitting the actual PAN.

As an example, when a customer purchases a coffee via a mobile app or renews a monthly digital subscription, the true PAN gets instantly replaced with a randomly generated token that enables a safe transaction.

The token is unique to one card, one merchant, and one device at a time. With tokenized payments, the actual PAN is never transmitted during the transaction, making the payment exponentially more secure. This is the key functional strength of tokenization as a security measure.

Reducing Compliance Scope

Storing tokens instead of raw PANs is the primary alternative for reducing the massive footprint of cardholder data in an environment, which directly helps in reducing a merchant’s effort to implement rigorous PCI DSS 4.0 requirements.

It is worth clarifying that tokenization solutions do not completely eliminate the need to maintain and validate PCI DSS compliance, but they can certainly simplify a merchant’s validation effort by drastically reducing the number of physical and virtual system components pulled under PCI DSS scope. Besides, by eliminating the operational need to store actual card numbers and other sensitive information, tokenization can significantly reduce the compliance risk and financial liability associated with data breaches.

How Does Tokenization Work?

Payment card tokenization works by replacing a cardholder’s true PAN with a one-time, unique identifier. These randomly generated tokens act as a secure stand-in for sensitive data that communicates exactly where the payment request is being routed from.

The steps below summarize how tokenization actively works during a transaction:

- Collection of Payment Data: The customer initiates a purchase with the merchant, providing their physical payment card details or digital wallet at checkout.

- Token Generation: The PAN provided by the customer gets converted into a secure “Token.” A token can be pre-generated when the customer provides explicit consent to the merchant to tokenize and store the card for future use. It can be generated for single-use or multi-use (meaning the token is used to represent a PAN across multiple recurring transactions). The bottom line is that the point-of-sale (POS) system or payment gateway uses the token as the card number instead of the customer’s true PAN.

- Token Processing: Once the token is created, it gets securely transmitted to the Issuer bank or token service provider (TSP), who holds the secure mapping in a highly fortified card vault to authenticate and authorize the transaction. The process of retrieving the true PAN from the token is called De-tokenization.

- Authorization Request: Once the transaction has been authorized by the issuer, the PAN is again mapped to the token to generate the authentication response containing the encrypted token, which is then sent back to the Merchant via the payment channel.

- Transaction Completion: Based on the authorization response, a transaction can be approved or declined by the issuer bank. In the case of a successful transaction, the payment gateway redirects the user to the merchant interface for immediate confirmation of payment.

How Are Tokens Generated?

When viewed from a merchant’s technical perspective, there are multiple cryptographic ways in which a token can be generated and utilized. A few of the token generation approaches that are commonly used include:

- Using a highly reversible cryptographic function paired with strong, centralized cryptographic key management.

- Implementing a one-way, non-reversible cryptographic function (i.e., a strong keyed hash algorithm).

- Deriving a token from a specific index function, sequence number, or even a randomly generated number that is entirely independent of a mathematical function.

It is further interesting to note that tokenization is available in many sizes and structural formats:

- An actual PAN (

4234 5678 9124 3456) can be converted to an alphanumeric string (7aF1Zx158674mwy6wl5x2). - A PAN (

4256 0068 0152 3398) can be converted to a purely numeric string (727629118523184563129). - Also, a token can consist of a truncated PAN in which the first 6 and last 4 digits are retained for routing purposes, however, the highly sensitive middle digits are completely replaced with alpha-numeric characters.

Unlocking the Power of Tokenization: The Role of Training

Tokenization is continuously evolving to meet emerging global security challenges and rapid technological advancements. Ongoing efforts are being made by card brands to establish common global tokenization standards, enabling seamless interoperability and simplifying integration across disparate payment platforms. Advancements in tokenization technologies, such as dynamic tokens and biometric authentication, will further strengthen card payment security. Businesses that proactively adopt tokenization as a foundational security measure will be at the forefront of creating a safe and secure payment environment.

To master these complexities, SISA’S flagship training workshops, such as the CPISI training program, cover tokenization in much more granular detail and offer a comprehensive understanding of the latest version of the Payment Card Industry Data Security Standard.

The training delves directly into the deep technical aspects of tokenization, such as token generation, vaulted storage, and usage, as well as the associated security controls strictly required to maintain audit compliance. It highlights the critical importance of selecting robust tokenization solutions, securing the underlying tokenization infrastructure, and intelligently integrating tokenization with other advanced security measures like Managed Detection and Response (MDR).

Key Implementation Considerations

The underlying considerations stated below, when implementing tokenization (be it on-premises, outsourced to a tokenization vendor, or adopting a hybrid approach) help organizations appreciate the significance of tokenization within the context of overall data security and continuous compliance:

- Strict Scoping: All system components, operational processes, and people involved in the tokenization and de-tokenization process must be included in the formal PCI DSS scope and heavily segmented from untrusted, out-of-scope corporate networks. Any system with the ability to access true PAN data or the operational ability to retrieve a PAN from a token must be included in the PCI DSS audit scope.

- Secure Vaulting: The tokens must be generated and processed within a highly secure tokenization system, and any mapping between the PAN and the token must be stored within a secure card data vault, implemented with applicable high-grade security controls as per PCI DSS requirements. Finding these rogue PANs before an audit requires a robust data discovery and classification tool.

- Secure Transmission: The communication channel between the tokenization system and the requesting application must be flawlessly secure to prevent any possibility of capturing the PAN, the Token, or the mapping database by an attacker. The mandatory use of strong cryptography and protocols (like TLS 1.2 or higher) during the storage and transmission of the data is highly recommended.

- Clear Distinction: The entity must maintain a programmatic mechanism to clearly distinguish between stored tokens and actual PANs.

- Hardened Configurations: All system components should be tightly configured as per industry-standard benchmarks (such as CIS) to completely eliminate known vulnerabilities.

- Continuous Monitoring: Strong logging, alerting, and continuous monitoring controls must be implemented across the tokenization boundary.

- Access Control: Access to the tokenization system and the cardholder vault must be strictly controlled by implementing a robust, zero-trust Identity and Access Management (IAM) policy.

Finally, while working with a third-party tokenization vendor or payment gateway, their official PCI-DSS compliance status (AOC) must be strictly verified during onboarding, and the entity must maintain a comprehensive service agreement with security and breach notification clauses being clearly defined.